As bitcoin continues to grow in popularity, the need for clear and consistent reporting requirements becomes more pressing for both taxpayers and tax authorities. With the IRS increasing its focus on digital assets, you might wonder how upcoming tax reporting changes will affect you. Don’t worry—this article breaks down the key updates and what you need to do to stay compliant.

Key changes ahead: What you need to know

The IRS is introducing significant updates in two main areas:

- New tax forms: 1099-DA

Starting in the 2025 tax year, exchanges will be required to issue a new form called the 1099-DA (Digital Assets). This form will include crucial information like acquisition and sale dates, proceeds, and cost basis of digital assets disposed of during the 2025 tax year, helping to standardize tax reporting for bitcoin moving forward. - Cost basis calculations

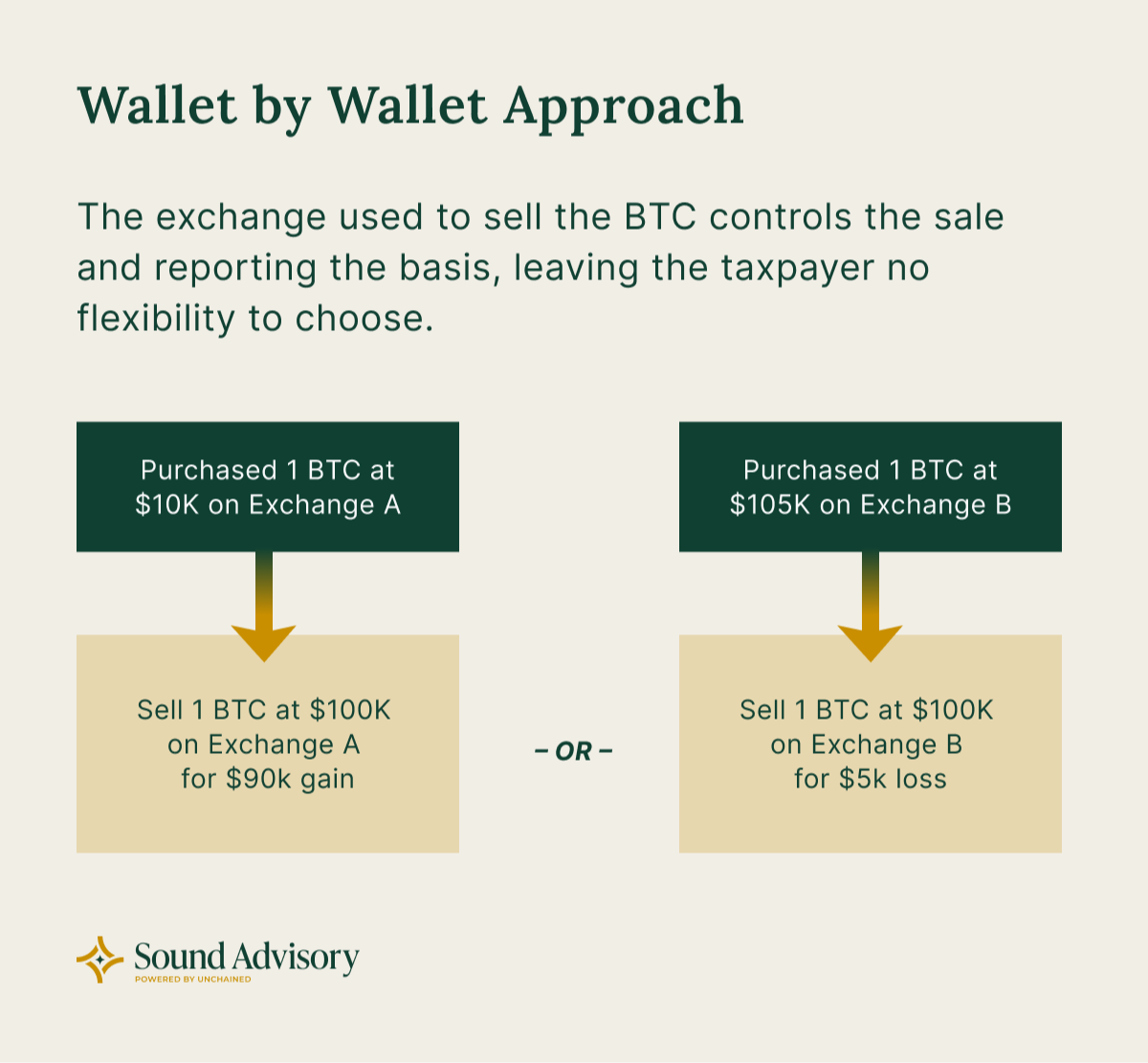

The IRS is eliminating the “universal wallet” approach and replacing it with a “wallet-by-wallet” tracking system for digital assets. This means the basis reported on sales must match to purchases made in the same wallet or exchange.

Understanding the shift: “Universal Wallet” to “Wallet-by-Wallet”

What is the Universal Wallet Approach? The universal wallet approach allowed taxpayers to combine assets from multiple wallets into a single "pool" for tax reporting and allocate basis to disposed assets regardless of what exchange assets were purchased or sold on. However, the IRS is now requiring a different standard for reporting, requiring taxpayers to track assets on a wallet-by-wallet basis, ultimately requiring separate records to be kept for each exchange the taxpayer uses.

Why is this change happening?

These changes ultimately reflect the IRS’s effort to create a robust framework for taxing digital assets effectively and fairly:

- Enhanced transparency: The IRS aims to close gaps in cryptocurrency tax compliance by introducing more precise tracking and reporting requirements. These rules ensure that gains and losses are reported accurately.

- Improved compliance: By standardizing the cost basis reporting through wallet-by-wallet tracking and requiring exchanges to issue Form 1099-DA, the IRS seeks to simplify and enforce compliance for both taxpayers and exchanges.

- Modernizing tax regulations: As digital assets become mainstream, these rules hope to bring tax regulations in line with other financial instruments, showing the IRS can adapt to evolving technologies and markets.

How this will affect you

This change will significantly impact those who buy and hold their bitcoin across multiple exchanges. However, anyone who has taken custody of their bitcoin (is holding their keys) will have fewer changes to adapt to.

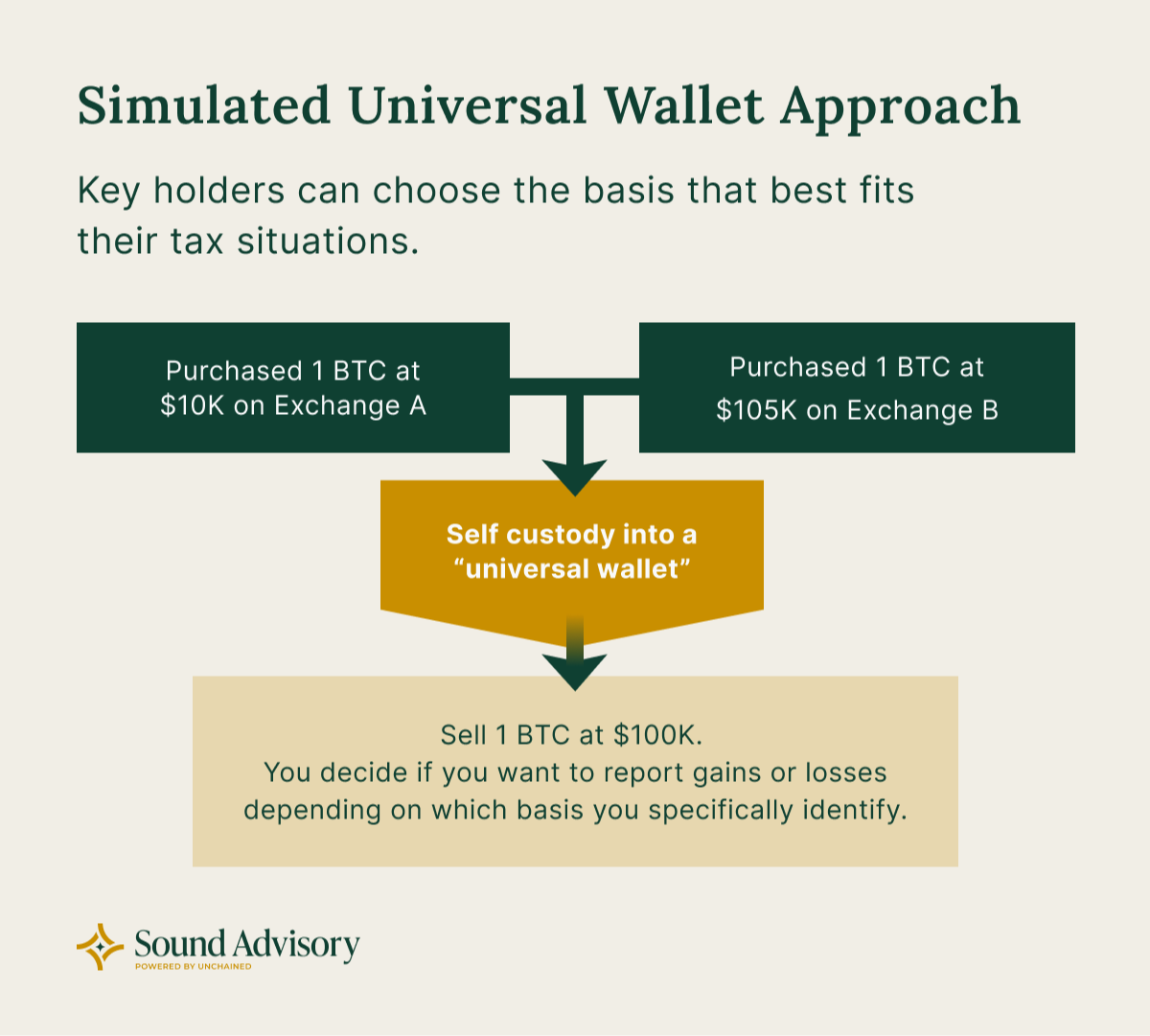

Luckily, you can - and many readers already have - simulate a “Universal Wallet” by taking custody of your coins into a single wallet, off-exchange. Imagine you purchased 2 BTC through 2 separate exchanges; the diagram below shows the new regulations in action based on the “Wallet-by-wallet” approach and the simulated “Universal wallet” approach through key control.

If you’ve taken custody of your bitcoin, you’re likely already accustomed to managing cost basis on your own. Prior to these changes, the IRS had indicated that it is the taxpayer’s responsibility to track the cost basis and identify which lot of coins you’re selling when you report sales to the IRS. The new rules may not significantly affect you, as your wallet doesn’t track this information for you—this responsibility falls on you as the taxpayer.

Many have used specific identification methods to assign cost basis, allowing them to optimize their tax strategies. With the upcoming changes, you’ll likely choose to continue using this method.

If you’ve been using an exchange, the new IRS rules could require you to keep separate, detailed records of each transaction across different platforms. Exchanges have not historically been required to track cost basis information, so you’ll need to be proactive in ensuring accurate information for tax reporting on assets purchased before December 31, 2024.

The 1099-DA will be a helpful resource for standardizing tax reporting, but it’s crucial to understand that the exchanges may not always report your basis accurately, especially if you’ve moved bitcoin between wallets or platforms. If you’ve sold bitcoins that were transferred between exchanges or wallets, you may need to track and calculate the basis for each transaction manually.

How to prepare for the changes

Safe Harbor allocation plans

The IRS offers a Safe Harbor Protection via Revenue Procedure 2024-28, which allows taxpayers to allocate unused cost basis as of Jan 1, 2025, using either:

- Specific identification – granular level tracking, assigning specific cost basis amounts to individual purchases of bitcoin based on the price and date of each transaction.

- Global allocation – Applies a consistent rule to all assets held as of December 31, 2024. This approach will limit your ability to make strategic tax decisions based on which bitcoin you want to dispose of in a given transaction. Someone may want to gift their lowest basis coins while selling their highest basis coins.

To meet the IRS safe harbor criteria, taxpayers must adopt the specific identification method by the earlier of the first sale, transfer, or disposition in 2025, or the due date of their 2025 tax return (including extensions). To use the global allocation method, taxpayers must describe their intended global allocation approach before January 1, 2025.

You’ve likely used the specific identification method for your bitcoin dispositions in years past. Not only is this often the most optimal tax strategy, but it also gives taxpayers the maximum time to organize their records. While it may require additional effort, it can result in substantial tax benefits depending on how and why the bitcoin was disposed of.

Anticipating the challenges ahead

As with any significant regulatory change, there will be some growing pains. Taxpayers who haven’t been meticulous about tracking their bitcoin or who have spread their holdings across multiple wallets may find the transition difficult. The IRS’s move to wallet-by-wallet reporting means that more detailed tracking will be required to ensure that every sale is accounted for properly.

The transition should be relatively smooth for those who have consistently managed their wallets and kept good records. However, for others, this shift could add extra complexity to their tax reporting.

Final thoughts: Stay ahead of the curve

The Revenue Procedure contains some areas of uncertainty, prompting the American Institute of CPAs to request additional guidance, which could be issued at any time. The information in this article reflects the current interpretation of the available guidance and what is considered the optimal tax approach. The regulations set forth by the IRS represent a significant shift toward more rigorous and transparent reporting. By organizing your wallets and maintaining accurate records of your purchases and sales, you’ll be well-prepared to handle the changes coming in 2025 and beyond.

Remember, accurate recordkeeping and proactive planning are key to staying compliant. If you need help understanding these new rules or preparing for the safe harbor election, book an intro with Sound Advisory. We are here to ensure you’re ready for tax season and beyond.

Revision: IRS Notice 2025-7

On December 31, 2024, the IRS issued Notice 2025-7, which provides a temporary relief period for taxpayers holding digital assets with brokers or exchanges. This relief aims to help address the challenges these brokers and exchanges face in implementing systems that allow customers to identify the basis of their digital assets rather than defaulting to the First-In-First-Out (FIFO) method. Taxpayers who custody their own Bitcoin are unaffected by this notice and must still adhere to the requirements outlined in Revenue Procedure 2024-28. Since the primary focus of Notice 2025-7 is to resolve issues specific to brokers, it introduces no new rules for self-custody.